Why Invest?

Bro-fest: A mini-history of capitalism in the United States

What are financial markets, exactly?

What does it mean to be a responsible investment?

How to invest responsibly

What your financial advisor doesn’t want you to know

There’s more than fifty trillion dollars swimming around in the global ocean of financial assets. That’s two and a half times the US GDP on a good day. Right now (2020), women in American control just over $10 trillion dollars. By 2030, women will control more than $30 trillion in financial assets. Because women live longer than men, ha. Patience prevails, sometimes.

There’s a whole lot of billionaires in this country. But it’s up to us to decide who becomes the first trillionaire, or be radical and decide there shouldn’t be a trillionaire. Maybe we can pool our money and influence and get rid of billionaires while we’re on a roll. Since when did you get to decide who becomes a billionaire or a trillionaire? Well, today!

Your 401(k) or retirement account might not feel powerful and able to break the kneecaps of the worlds biggest piggybanks, but we can do it together. This is our Rosie the Riveter moment, ladies. Our 401(k)s and IRAs are powerful beyond measure. $10 Trillion is a whole lot more than Jeff Bezos has got – almost fifty times more. He gets richer because WE ALLOW IT.

So, you’re on board with this whole bring em’ to their knees idea. But now what? Well, let’s start somewhere. Let’s start at the beginning.

Why Invest?

Investing gets lots of attention, and there’s no shortage of websites and people who will take your money, teach you the “game”, and pound the principles of investing into your head.

But why?

Because you’ll fall behind by doing nothing.

That’s right. Saving isn’t enough. You save to secure your future. You save to not be a bag lady. You don’t want to couch surf at 85, or travel coach at 75, for that matter. You might have $50K sitting in a savings account right now, your 401(k) invested in a money market fund, or an inheritance you’re afraid of losing – that’s in cash too. Just because it feels good doesn’t mean it’s good for you.

There’s really good reasons for sitting on cash, like having an emergency fund, savings for a house or wedding or that self-funded sabbatical. But these are all short-term things you’re saving for. You can’t save for the future the same way you save for tomorrow or next year.

Because, inflation.

Inflation is like having a cookie everyday. It’s sweet until you realize you’ve gained ten pounds. It just creeps up on you. Except that inflation takes so damn long to do it’s creep that when we’re talking about your money and your retirement, you don’t even realize it’s happening until it’s too late.

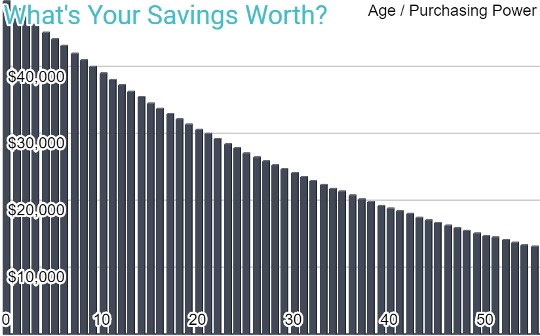

Purchasing Power

It’s really hard to visualize how much you lose to inflation, and the name it’s given doesn’t help much. Purchasing power is not just financial feminism. It’s how far your dollars will stretch at some far-off day in the future when you’re no longer earning money and rather, spending it. Purchasing power is painfully clear at 75. Not so much at 35 or 45. If you have $50,000 in savings today and don’t touch it, it’ll be worth about half as much in 30 years.

It might feel really good to have a big savings account, and hey, I’m right there with you! But, at a certain point, the savings account will come back to haunt you. Why? Because each and every day it loses a little bit of it’s value, and you have no idea, because the number stays the same. But it’s NOT the same. It’s less. Ubers will cost double what they used to be, and your healthcare… forget about it. The tooth fairy will be putting 20 dollar bills under pillows when you’re claiming social security.

Investing is basically long-term savings. It allows your money to keep pace with inflation, the cost of avocado toast and your gym membership. This is the most basic, and most appropriate way to look at investing. It allows you to have the same lifestyle at 75 that you had at 45, when you’re in your prime earning years. Investing is not a means to build wealth, but to preserve wealth.

If you don’t want to be a bag lady, then you must invest. If you’re concerned about your future self, then you must invest. If you worked hard for the money you earned, then don’t squander it in a savings account. Invest it.

It’s really that simple.

It sounds scary because investing can be a bro-fest of day traders, technical analysis, and complicated ratios and numbers. It also means you can “lose” money when markets tank (only if you pull it out!), but that’s why it’s long-term. You’ll lose more money than you could possibly imagine by doing nothing, which is exactly what a savings account does for you, at least for the foreseeable future.

Bro-fest: A mini-history of capitalism in the United States

Why am I taking your precious time to explain our economic system in a guide to responsible investing? Because there’s the band-aid solutions in life, and then there’s addressing the root cause of a problem. A little historical context is worth knowing to understand how we got to where we are. And if we’re in this place by design, it’s going to take a thoughtful re-design to change things.

The daddy of American capitalism is Adam Smith, who believed that self-interest benefits everyone in the end. That pretty much invalidates the economic contribution of every caregiver in history. Follow him up with Milton Friedman, who thought that women shouldn’t be paid equally because it’s inefficient.

This pretty much sums up our economic system today, and Adam clearly forgot the selfless interests that were cooking his dinner and washing his laundry as part of the equation. The capitalism we have today favors profits, not people, and definitely not women (or any other marginalized demographic). Women haven’t been compensated for their domestic labor, were treated as property in marriage contracts, and barred from the same rights, education, and access to economic opportunities throughout our history.

Capitalism was created by a man who profited from the free labor of women.

This makes perfect sense, because Adam Smith determined that the government should have a limited scope of oversight, namely national defense, law and order, basic infrastructure like roads and public education designed to create non-thinkers, btw. Nevermind that his entire economic system was built upon the silent, unpaid work of half the population. To be fair, Smith was against the unpaid effort of slavery, if primarily for economic reasons, so there’s that to be glad about.

Social welfare systems benefit women and people of color more than (white) men, and so of course our country is vehemently against them in the name of “capitalism”. And while you might find me to be decidedly “anti-capitalist”, I’m just your run-of-the-mill person who gives a shit about human welfare, and happens to think there’s a better way of actually implementing capitalism (ahem, Scandinavia!) than our compassionate approach of work until you die, or die.

At the heart of Adam Smith’s capitalism is shareholder value, essentially that a company’s primary responsibility is to generate returns for shareholders. Not a shareholder, not my problem.

Except that 84 percent of all stocks owned by Americans belong to the wealthiest 10 percent of households.

This is not good on so many levels, but there is a huge opportunity for women to reshape capitalism as we know it, if you’re in the 10%. If you are in that 10%, you will hold power we never dreamed of 100 years ago. Because money buys politicians. Money buys regulation. Money buys change. And if you’re in that 10%, you have a moral obligation to harness that power for the good of those who cannot.

Tilting regulation towards equity, equality and social services generally costs more or otherwise said earns less profit for today’s shareholders. But it won’t for the shareholders of the future, who are increasingly female and the ones most likely to use the services that increase the chances that women and other marginalized populations can compete on a level playing field.

So if you don’t have an economic imperative to invest, now you have a philosophical one.

Let’s move on to financial markets and how they work, now that you understand the importance of being an educated investor for the wellbeing of your future and our collective future.

https://www.nber.org/papers/w24085.pdf

https://www.nytimes.com/2018/02/08/business/economy/stocks-economy.html

What are financial markets?

Financial markets are the equivalent of supermarkets for companies. You go in with your list, buy what you need, and walk out. You don’t go to the baker or dairy farm directly, or to the ketchup manufacturer. The grocery store is the broker, literally housing the goods they think you want to buy. Financial markets are the shopkeepers for thousands of publicly traded companies that wanted an injection of outside investor money at some point in time. Instead of contacting their investor relations department directly, you just swing into the financial supermarket and pick up a little of this, a little of that. Ideally, you’re doing the outside aisle sweep, picking up the whole foods, unprocessed items, and skipping the inner aisles with the (literally) toxic options.

Just like there’s a number of grocery stores, each one catering to a different market, there’s different financial markets too. They’re the names you’ve heard like the Dow Jones, S&P 500, and the NASDAQ. The Dow is the original financial market and represents just 30 of the largest/important companies in the United States. The S&P 500 is a little more egalitarian and has 500 and is supposedly a more diverse representation of US companies, and finally the NASDAQ caters to tech companies. You won’t go to Whole Foods expecting high fructose corn syrup in your products, just like you don’t buy NASDAQ stocks expecting lots of dividends and steady growth. Who decides what’s in each financial marketplace? Just some committee of “experts” who are probably exceeding white, male, and aged. They all claim to be very transparent on their websites, but good luck finding actual diversity metrics!

These are just a few examples of financial “marketplaces”, and there’s a whole bunch more in the US and globally. In fact, there’s millions of them (approximately 3.5 million, if you care to know). It’s ironic, given that globally there’s just about fifty thousand public companies (and about 5,000 in the US). If you find investing overwhelming, this might be one reason why! For every publicly traded company, there’s over 70 “markets” to buy the product at. Your financial grocery list is the equivalent of hitting up every store in town on very specific days and times to maximize your coupon game. I.e., it is a full time job.

And just like our good old food pyramid, your investment portfolio needs to be balanced, too.

It might feel good to have a bunch of “winners” but need I say more than Blockbuster and AOL? Because we don’t know if the next winners are coming from the US or Azerbaijan, from a tech company or a startup that desalinates ocean water safely and cheaply, we don’t put all our eggs in one basket. We spread out our investments proportional to the global economy and trust that everything balances out, in the end.

The missing question.

The missing question in this financial markets discussion is asking who’s profiting from this system and who’s not? Who exactly decides which companies get to be publicly traded? How did startups go from Jeff Bezos in their garage to a stock market over-achiever? Why do so many businesses fail or stay forever small, and others succeed?

Is it raw talent, drive, and hustle that makes the publicly traded companies “better” somehow? Are the failing companies lazy, do-nothings that don’t know how to manage a business?

Keep reading, my friend.

What is responsible investing?

First of all, is there such a thing as a responsible, ethical company? If we revisit our economics lesson, we have our answer. It depends on who you ask, and how they define “responsible”. The owner of Amazon thinks himself highly responsible by timing warehouse worker productivity down to the second so he can squeeze out a penny more of profit per share off the backs of low paid laborers. That is the corporate definition of delivering shareholder value.

Ask the part-time employee of any large multinational corporation how they feel about working two jobs (or more) to barely pay for rent, healthcare, and food, and they might disagree with the above sentiment.

Enter stakeholder capitalism.

Stakeholder capitalism is an attempt to shift the narrative. From shareholder to stakeholders, from investor to the person whose labor makes your morning cereal possible. From output to the environmental impact on the town the manufacturing plant resides in and the wellbeing of its community.

Sadly, stakeholder capitalism, however elevated in idea, is rarely

- History of sustainable investing

- Greenwashing

- Types of responsible investments

- What matters to YOU?

How to invest your values(include recommendations)

- What matters most?

- Doing your due diligence

- Finding resources to help you

- Questions to ask

Responsible Spending

- What your financial advisor doesn’t want you to know

- The fastest way to make an impact

- Which return matters most?

- Total Impact